- Services

Auditor-Focused Evidence Map

Emissions Avoidance Project

Purpose:

This evidence map is designed for external auditors, validators, internal audit teams, and assurance providers. It links each material project assertion to primary evidence, control owners, and audit tests, enabling efficient planning, walkthroughs, and substantive testing.

Asset Reference:

Project located in Los Angeles County, California, USA (onshore)

1. Core Assertions → Evidence → Audit Tests

A. Ownership & Control

Assertion: Jedon Kotler has singular authority over extraction decisions.

- Primary Evidence

- Mineral and subsurface rights deeds / title reports

- Operating agreements (if applicable)

- Corporate resolutions evidencing control

- Control Owner: Legal / Asset Management

- Audit Tests

- Inspect deeds and chain of title

- Confirm no conflicting operatorship rights

- Reconcile ownership across periods

B. Enforced Permanence (Non-Extraction)

Assertion: Emissions are permanently avoided because extraction is prohibited.

- Primary Evidence

- Binding forbearance / non-extraction instruments

- Operational prohibitions and restrictions

- Transfer constraints preserving non-extraction

- Control Owner: Legal / Compliance

- Audit Tests

- Inspect enforceability and duration clauses

- Verify restrictions survive transfer

- Confirm no carve-outs enabling production

C. Credible Baseline (Economic Viability)

Assertion: Avoidance is meaningful because production would be viable absent the project.

- Primary Evidence

- Independent reserve evaluation

- Historical production records

- Economic viability analysis

- Control Owner: Technical / Finance

- Audit Tests

- Validate independence and methodology of reserve report

- Trace historical data to source records

- Assess reasonableness of economic assumptions

D. Additionality

Assertion: Non-extraction is voluntary and not legally required.

- Primary Evidence

- Regulatory analysis confirming no production ban

- Internal decision documentation

- Control Owner: Legal / Compliance

- Audit Tests

- Inspect regulatory correspondence

- Confirm absence of mandates compelling non-production

E. Project Boundary & Scopes

Assertion: Avoided emissions cover lifecycle Scope 1, 2, and 3 impacts.

- Primary Evidence

- Project Design Document (PDD)

- Boundary definitions and scope rationale

- Control Owner: Technical / MRV

- Audit Tests

- Confirm boundary completeness and exclusions

- Reconcile scopes with lifecycle pathways

F. Quantification Methodology

Assertion: Avoided emissions are conservatively quantified and reproducible.

- Primary Evidence

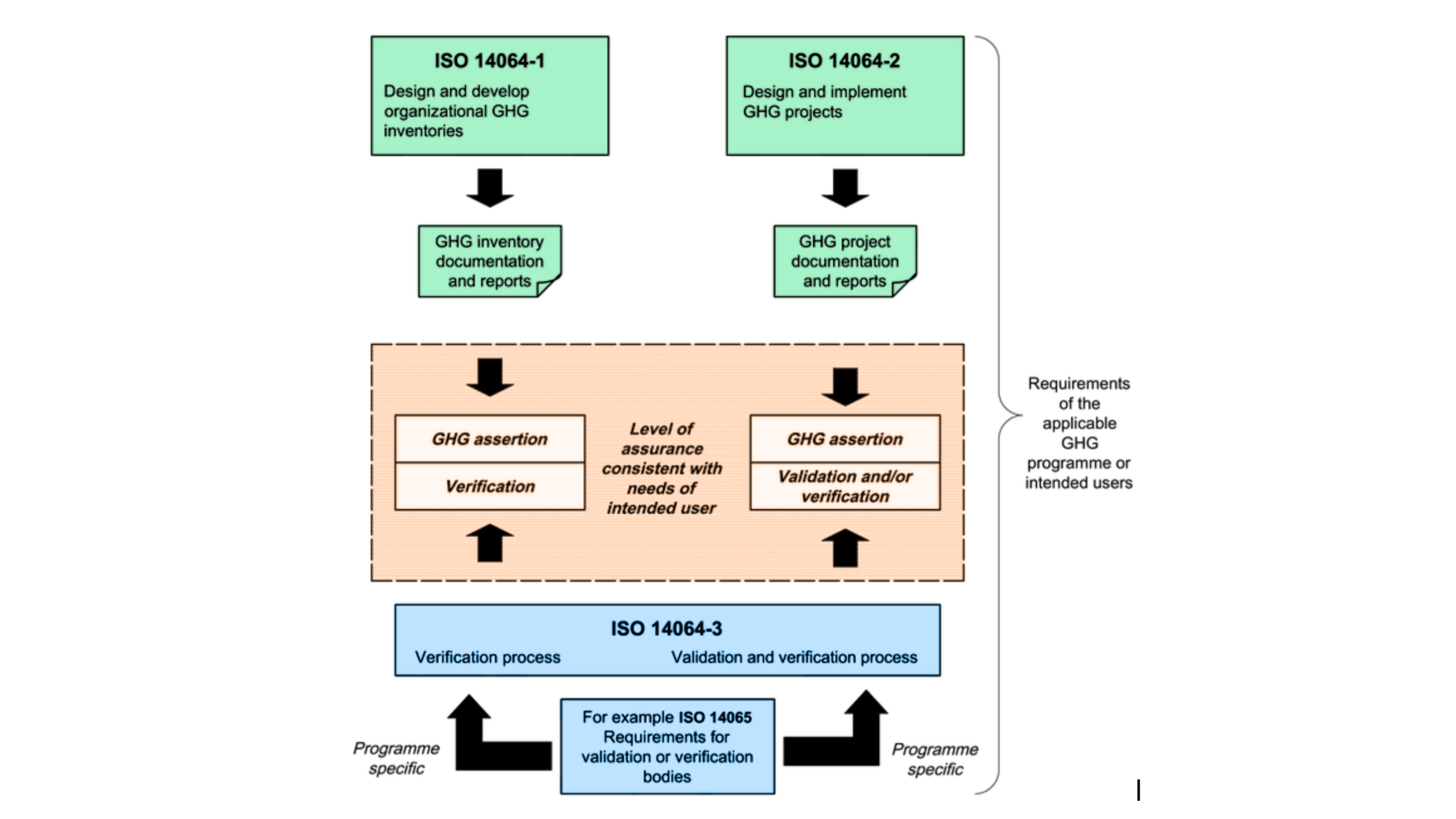

- Methodology document aligned to ISO 14064-2

- Calculation workpapers and parameters

- Emissions factor references

- Control Owner: Technical / MRV

- Audit Tests

- Reperform calculations from source data

- Assess conservativeness and uncertainty treatment

- Verify parameter sourcing and consistency

G. Independent Validation

Assertion: Methodology and application were independently validated.

- Primary Evidence

- ISO 14064-3 validation report

- Validator accreditation credentials

- Validation scope and findings

- Control Owner: Compliance / External Assurance

- Audit Tests

- Confirm validator independence and accreditation

- Review scope coverage and limitations

- Trace findings to underlying evidence

H. Monitoring & Ongoing Status

Assertion: Continued non-extraction is confirmed over time.

- Primary Evidence

- Periodic status attestations

- Monitoring logs confirming absence of production

- Ownership and boundary confirmations

- Control Owner: Compliance / Asset Management

- Audit Tests

- Inspect monitoring cadence and records

- Confirm no production permits or activity

- Reconcile ownership continuity

I. Double Counting Prevention

Assertion: No parallel claims exist.

- Primary Evidence

- Claim control statements

- Registry non-participation disclosures (if applicable)

- Transaction records

- Control Owner: Legal / Compliance

- Audit Tests

- Inspect claim exclusivity documentation

- Confirm absence of overlapping registry entries

J. Disclosure Discipline

Assertion: Public claims do not exceed validated evidence.

- Primary Evidence

- Website and marketing content

- Disclosure policy and approvals

- Claim limitation statements

- Control Owner: Compliance / Communications

- Audit Tests

- Compare public claims to validation scope

- Compare public claims to validation scope

Identify and flag over-statement risk

2. Audit Planning Shortcuts

- Key Controls: Ownership documentation; non-extraction instruments; validation report

- Highest Judgment Areas: Baseline viability; Scope 3 factors; uncertainty treatment

- Low-Risk Areas: Reversal (structurally eliminated); operational performance (no activity)

3. Evidence Readiness & Retention

- Version Control: All primary documents versioned and dated

- Retention: Maintained for retrospective review and discovery readiness

- Access: Provided under NDA / assurance protocols

Auditor-Focused Evidence Map

4. Auditor Conclusion Guide

An auditor should be able to conclude, with reasonable assurance, that:

- The emissions-avoidance claim is ownership-enforced

- Permanence is structural, not probabilistic

- Quantification is conservative and reproducible

- Validation is independent and appropriately scoped

Public disclosures are aligned with evidence